How Gaming Became the New Social Network, Theme Park, and Music Festival

Why Gaming Is The Most Underrated Industry

This is a weekly newsletter about tech, media, and culture. To receive this newsletter in your inbox each week, you can subscribe here:

Game On: Virtual Worlds and the Future of Gaming

Last month, my 13-year-old cousin asked for a flyable, rideable neon parrot for her birthday.

If you’re not familiar with a flyable, rideable neon parrot, (1) I don’t blame you, and (2) it’s a type of pet that you can care for in the Roblox game “Adopt Me!”. More than any gift in the world, my cousin wanted a virtual pet in Roblox.

(A side note: yesterday, Roblox launched a venue for virtual birthday parties—unfortunately for my cousin, she’ll have to wait until next year.)

Roblox, Minecraft, and Fortnite—three of the major MMOs (massively multiplayer online games)—each attract ~125M MAUs for ~1.5 billion hours of monthly playtime. Among 8-to-18-year-olds in the U.S., 8 in 10 have played Roblox.

But relative to its influence, gaming is incredibly underrated. Consider the size of the gaming market alongside more talked-about markets:

Even on a unit level, gaming operates on a scale that it doesn’t get credit for. Last year, Avengers: Endgame broke the record for a movie’s opening weekend, grossing $858M. Meanwhile, back in 2013, Grand Theft Auto V grossed over $1B in its first three days.

In order to show why gaming is (still) underhyped, I’m going to look at:

How gaming platforms are the new social networks,

The future for immersive virtual worlds,

The shift to user-generated gaming platforms,

Why new technologies will first show up in gaming, and

How gaming is leading the way for business model innovation across tech.

Then, I’ll look at three early-stage, three growth-stage, and three late-stage gaming startups worth watching.

1️⃣ The New Social Networks

Nineties kids came home from school and logged onto AOL Instant Messenger. In the 2000s, kids chatted with friends on Myspace and Facebook. Today’s kids hang out in Fortnite, Roblox, and Minecraft.

Games increasingly don’t have a purpose beyond socializing. Last year, Grand Theft Auto introduced a casino that was irrelevant to the game, only serving as a place for players to hang out. Earlier this year, Fortnite launched Party Royale as a new game mode exclusively for socializing. Roblox hopes its virtual birthday parties will accomplish the same.

It’s important to note that gaming isn’t only for teenagers. The average age of a U.S. gamer is 35; only 29% of gamers are under 18. As a generation of gamers has aged, gaming has been destigmatized: gaming is a natural way for billions of people around the world to socialize together.

The trend toward games as social networks has two key accelerants:

Cloud gaming allows players to access games from anywhere. In a previous generation, games had to be played on a console or a desktop. Today, players can move seamlessly between devices.

And with better tech, game worlds have become more immersive. It’s easier to hang out with friends in a virtual world that feels real and that facilitates these interactions.

2️⃣ Virtual, Cross-Cultural Worlds

Gaming’s cultural footprint has always loomed large: the highest-grossing franchise of all time isn’t Star Wars or Marvel or Harry Potter, but Pokémon. But increasingly, gaming is the medium through which people experience elements of culture.

Take Fortnite’s recent events: 28M people “attended” Travis Scott’s concert, 11M people attended Marshmello’s, and 3M people watched the Star Wars event with JJ Abrams last fall.

In Fortnite, players can be their favorite pop culture characters. Players can attend the Star Wars event as Han Solo. IP owners are more than happy to make this possible: Disney introduced Marvel “skins” and the NFL provided NFL jerseys—both for free. Offering your IP in Fortnite creates powerful brand affinity.

Part of what enables these cultural experiences is that this generation’s “games” resemble virtual worlds more than they resemble Tetris or Mario Kart.

Games are already taking steps to become the “metaverse”—a term from the novel Snow Crash that describes a collective virtual shared space. (Matthew Ball has an excellent deep-dive on the metaverse here.) Take these examples of how virtual worlds are bleeding into our real world:

A cell phone built in Minecraft can now make a phone call to the real world

Early in the pandemic, Minecraft players recreated the hospitals that China was rapidly building in Wuhan

Students sent home by Covid-19 rebuilt their schools and held virtual graduation ceremonies in Roblox

There’s a black market for virtual goods for the Nintendo game Animal Crossing

Over time, virtual worlds will become more robust, complete with their own virtual economies, virtual events, and virtual experiences. And it will be the users who will build these worlds.

3️⃣ Gaming Platforms

From an investor standpoint, gaming has historically been a difficult sector to invest in. The best gaming companies were often centered around a hit game, which exposed the broader company to fad risk as games came in and out of favor.

Today’s most compelling gaming companies, by contrast, are platforms. Companies like Roblox and Minecraft don’t create any games—players create their own games and earn a share of revenue. This significantly derisks an investment: there are over 40 million games on Roblox, with the top 10 games representing only 30-40% of revenue.

Many Roblox developers are teenagers, with the top developers making over $100K a month. Game developers are an underrated example of the “passion economy” or “solopreneur” phenomenon at work. And the gaming companies are formalizing these career paths: Epic Games launched Epic Games Publishing this spring to finance developers.

With the shift toward platforms, gaming companies have become technology companies more than media companies. Gaming is, at its core, an application of (often advanced) technology. Increasingly, it’s that technology, rather than any hit game, that forms a gaming company’s moat.

4️⃣ Emergent Technologies

Lines are blurring between gaming and tech. Is Roblox a gaming company, or is it an advanced virtual world that has game development capabilities?

This distinction will only become less clear. As games become technically more complex and immersive, gaming companies are at the vanguard of emergent tech.

Take the two largest game engines, Unreal and Unity. Unreal, Epic Games’ engine, was used to create The Mandalorian for Disney+. Unity, meanwhile, rendered the “live-action” Lion King. These engines are incredibly advanced. Check out these stunningly realistic renderings of human faces using the Unreal Engine—from 2016, 2017, and 2018:

Game engines have become so sophisticated that they’re used to power huge swaths of entertainment; soon, that influence will expand beyond entertainment into healthcare, education, and the workplace.

Gaming is also a leading candidate to develop a breakthrough VR / AR technology. Games have already shown that they can drive consumer adoption: Pokémon Go made AR mainstream and has grossed over $3B for Niantic. It’s easy to imagine a company like Epic Games or Roblox introducing increasingly immersive features, until virtual game worlds become full VR experiences. The next major computing platform may emerge from a game.

Just taking a quick breather to remind you to subscribe if you haven’t already!

5️⃣ Business Model Innovations

In 2019, Fortnite brought in nearly $2B in revenue. Yet Fortnite is free to play and doesn’t serve ads. Instead, Fortnite makes money from voluntary in-game purchases. None of these purchases are needed to play the game, to advance in the game, or to win the game. Instead, they’re cosmetic—costumes for your avatar, for instance.

Fortnite has proven this model works: its ARPU is more than the combined ARPU of Snapchat, Twitter, Facebook, and Google.

This business model is analogous to Chinese tech companies, which often have multiple revenue streams—tipping, subscriptions, ads, in-app transactions. Top Western games are following suit. The trend extends to gaming-adjacent companies: the chat platform Discord, for example, eschews ads in favor of a freemium model.

These models work at scale. Of Tencent’s $54B revenue in 2019, over 60% came from gaming—more than triple the revenue from either advertising or payments. Facebook, meanwhile, makes 97% of its revenue from ads.

The trend toward non-advertising monetization is being met with a growing Western backlash to ad-based business models. Gaming is leading the way in business model innovation. The next generation of consumer tech companies will have business models that resemble Fortnite’s more than they resemble Facebook’s.

💡 Startups to Watch

These are gaming startups that I find especially compelling.

Among early-stage startups, Network Next is an interesting pick-and-shovel that improves underlying game performance. Playable Worlds, founded by a gaming veteran from Sony, is building an MMO specifically for socializing. And Guilded aims to be a new-and-improved Discord.

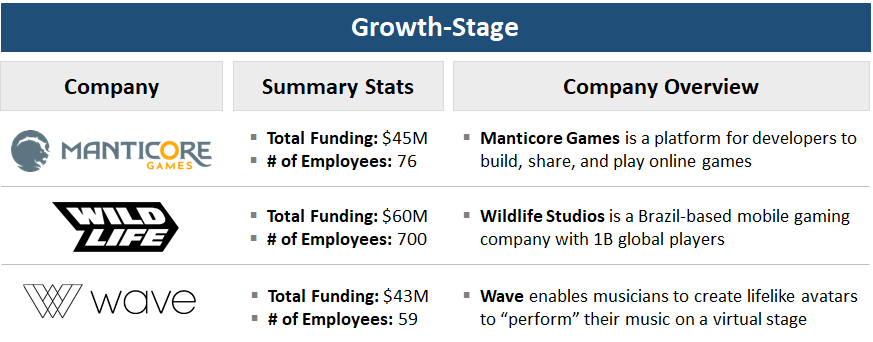

Among growth-stage startups, Manticore Games operates a platform called Core that aims to be one-stop-shop for game developers. Wildlife Studios has launched over 60 mobile games in 115 countries; ~50% of the game market is on mobile. And Wave builds the tools for in-game virtual performances.

Within late-stage startups, Discord has 300M users (4x from 2018) and 100M active users (+50% YoY), making it about a third the size of Twitter or Snapchat. Roblox hit $103M in May revenue ($1.2B run-rate) and paid out $100M to developers last year. Improbable powers the virtual worlds in MMOs.

Final Thoughts

Gaming in 2020 is unrecognizable from gaming in 2010. While gaming companies in the past resembled media companies and produced content, the industry’s leaders today are platforms, social networks, and powerful tech engines.

I’ll go out on a limb and say that if a new company joins the ranks of FAANG by 2030, it will be a gaming company—a company like Epic Games or Roblox that creates an early version of the metaverse. Over the next decade, gaming will play a central role in culture and will be increasingly influential on the broader tech industry.

Sources & Additional Reading—here are the pieces that inspired and informed this content; check them out for further reading on this subject:

Much of my thinking on gaming has been shaped by Matthew Ball’s writing—I recommend all of his pieces, which you can find here

Six Trends Revolutionizing Gaming | Jonathan Lai & Andrew Chen | a16z

A Multiverse, Not the Metaverse | Eric Pickham | TechCrunch

Chart of the Week

There’s a Lenin quote that goes:

There are decades where nothing happens; and there are weeks where decades happen.

It took a decade for e-commerce penetration to increase 10 percentage points from 6% to 16%. It took eight weeks to gain the next 10 points. (Source)

📱 Tech

Why Figma Wins | Kevin Kwok

Kevin Kwok wrote an excellent analysis of Figma’s success. Some factors:

Design is bigger than designers: Figma’s core insight was to build a product for designers and for the other people involved in the design process (PMs, engineers, the CEO).

Cross-side network effects: That insight creates powerful compounding loops. Designers pull in non-designers. Those non-designers then encourage new designers to join.

Browser-first: Before Figma, file-sharing was done in the cloud (e.g., Dropbox), but the actual design process was not. Figma changed that and enabled real-time collaboration.

Bottom-up GTM: Like many collaboration software peers (including Airtable, where I work), Figma approached GTM bottom-up, spreading organically through companies.

In a related piece:

As someone who spends approximately 40% of my time at work wondering why G Suite is so bad, I liked this piece on how Google blew a 10-year lead in collaboration software. In 2010, Google Docs and Google Sheets seemed revolutionary (real-time collaboration? wow!); in 2020, they seem clunky, slow, and unimaginative.

What Comes After Zoom? & The Verticalization of Zoom | Benedict Evans & JJ Oslund

If there’s one product that will forever be associated with Covid-19, it will be Zoom. Zoom is now both a household name and a verb. Since January, Zoom’s market cap has grown from ~$20B to $73B.

But what’s been Zoom’s greatest strength—what’s enabled its growth—is also Zoom’s greatest weakness. By not needing an account or an app to join a Zoom, Zoom was able to grow virally during the pandemic. But that also means Zoom has no moat.

JJ Oslund sees the “verticalization of Zoom.” Video will be a commodity. Users will turn to Houseparty for social hangouts, Talkspace for therapy, and Tandem for a remote office.

I agree with his points, but it’s also worth noting that Zoom itself is becoming a platform. Marketplaces like Outschool are built on Zoom. And new software players like mmhmm and Macro are building products to improve the Zoom experience.

Online Dating During the Pandemic | Nilay Patel & Ashley Carman | The Verge

After spinning out of IAC earlier this year, Match Group is a standalone public company with a ~$25B market cap. Match owns 22 dating apps, including Hinge, OKCupid, Match.com, and Plenty of Fish—but its crown jewel is Tinder.

With 60M users, Tinder has more users than South Korea, Spain, or Italy. And it’s leveraged this user base to become the top-grossing mobile app in the world. This is despite ARPU of only $0.58. Tinder operates a freemium model, in which it upsells some customers to Tinder Pro and Tinder Gold (which unlock new features like undoing swipes, swiping in far-away places, and seeing who swiped right on you).

Tinder is an ever-growing portion of Match’s revenue:

Impressively, Tinder’s 32% operating margins are on par with Microsoft’s and Facebook’s (both 34%).

In a wide-ranging interview, the CEO of Tinder talks about how the pandemic is impacting online dating. Interestingly, he cites Fortnite as a key competitor: young people are beginning to have their avatars go on dates in virtual worlds.

The chart below shows how couples met over the last 80 years. Online dating sits at 40% today (for same-sex couples, it’s 70%).

The key question is when this curve will hit an asymptote—if it ever does.

🎥 Media

Netflix is Rewriting the Summer Blockbuster Script | Lucas Shaw | Bloomberg

This will be the first summer without a summer blockbuster since Jaws invented the phenomenon in 1975. But while theaters are empty, Netflix is redefining what “blockbuster” means. (I realize the irony of that last sentence, given what Netflix did to Blockbuster back in the 2000s.)

Over the last 20 years, action and adventure films grew from 35% of ticket sales to 60% of ticket sales. Comedies, meanwhile, atrophied from 25% to 7%.

This is where Netflix first seized its opportunity. While theaters focused on popcorn fare (e.g., Marvel film #73) and “safe” material (all 10 of the highest-grossing films last year were either comic book movies, sequels, or remakes), Netflix breathed new life into everything else.

Now, Netflix is infringing on the box office’s turf—right when the box office is most vulnerable. Not long ago, action stars like Chris Hemsworth and Mark Wahlberg would scoff at appearing in a direct-to-streaming film. Now, Hemsworth’s Extraction reached 100M households in its first month; Wahlberg’s Spenser Confidential reached 85M. For comparison, Black Panther sold 78M tickets during its entire theatrical run.

The Unbundling of News | Kia Kokalitcheva | Axios

Andrew Sullivan, one of New York Magazine’s top writers, announced last week that he’s leaving for Substack. Traditional journalism outlets like NYMag only just started to regain their footing after being decimated by the Internet; now, they’re fending off a new attack by Substack.

It’s interesting to think about whether this is the future of journalism: subscribing to your favorite writers, rather than to a broader publication.

For its part, Substack is providing the tools to enable this new economy: the company now offers writers healthcare, distribution, and even coworking spaces. This raises another interesting question: will horizontal platforms like Catch be the picks and shovels for disaggregated work, or will the vertical platforms themselves provide the underlying tools enabling these new careers?

🛍️ Commerce

How Costco Convinces Brands to Cannibalize Themselves | Adam Keesling | Napkin Math

Costco is the 14th-biggest company in the world by revenue, raking in $152B last year. In the midst of an Amazon-led retail apocalypse, Costco is thriving: over the past decade, it was the 2nd-fastest growing retailer in the world, ahead of even Amazon (only Lululemon grew faster).

Costco accomplishes this without making money from selling products. Costco sells its goods break-even, and then earns nearly 100% margin on its annual membership fee, which 100M shoppers pay for. (Check out this deck for more about Costco’s business model.)

Adam Keesling uncovers one more brilliant Costco innovation: the creation of Kirkland Signature, the best-selling private label brand in the world. While other retailers have many private label brands (Target and Walmart each have over 30), Costco has one brand across products; this has allowed the Kirkland brand to accrete in value for three decades.

But what’s most brilliant is that Costco convinces competitors to make Kirkland products. Kirkland Vodka, for example, is rumored to be made by Grey Goose. Why are brands willing to cannibalize their own product?

In short: the sheer volume of Costco sales. Costco is a coveted sales channels for a brand, and brands can still make money by making Kirkland products for Costco.

Quick Hits

🎼 The custom ringtone market grew from $68M in 2003 to $1.1B in 2007—a 100% CAGR. The Recording Industry Association of America even created awards for ringtone sales: Lil Wayne’s “Lollipop” went 5x platinum and is the best-selling ringtone of all time. From its 2007 peak, the industry has shrunk 97%. Ouch. (For what it’s worth—my first ringtone was Akon’s “Don’t Matter” on my Motorola Razr.) Link

✈️ Business travel makes up 60% to 70% of industry sales. Airlines are worried that it will never hit the same levels again. Link

📺 Netflix’s Chief Content Officer, Ted Sarandos, will now serve as co-CEO alongside Reed Hastings. This is emblematic of a shift Netflix has already made: Netflix is now more of a media company than a tech company—with a ~$20B content budget to show for it. Link

👂 Fresh off its $100M valuation, Clubhouse is drumming up excitement through exclusivity—3,500 users are in the beta, and even Oprah joined a recent event. Link

📹 Tencent is quietly testing Trovo, its Twitch competitor. Trovo closely resembles Twitch’s appearance and functionality. In April, Tencent spent $263M to buy control of Huya, China’s Twitch equivalent. Link

🛒 Amazon was the world’s top advertiser last year, spending $6.9B on ads. The rest of the top 5 was made up of Comcast ($6.1B), AT&T ($5.5B), P&G ($4.3B), and Disney ($3.2B). Link

Thanks for reading! To receive this newsletter in your inbox weekly, subscribe here 👇